Read Time: 4 Minutes

3 Factors That Determine Mortgage Qualification

When a bank or lender is deciding how much money they will lend you, they look at 3 pieces of information.

As a borrower, these are the 3 things you can control to maximize your borrowing power. After reading this you will understand what tweaks you can make, to ensure you appear your best to a lender when looking for a mortgage. Some of these things take time to improve, so knowing what they are and how they work is key well before going to a lender to ask for money. Be prepared, and understand what’s being looked at to ensure the best results.

Now, let’s dive in.

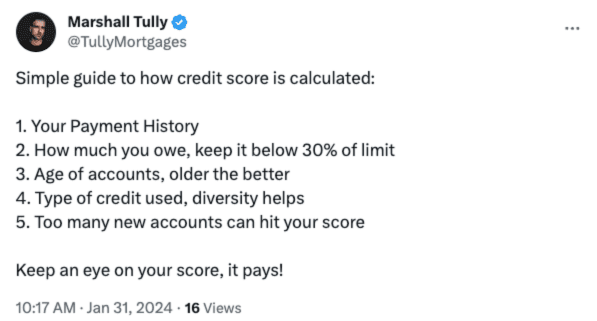

Credit Score and History

Your credit score is like your passport for lending, it will determine the type of lending you will get access to.

Scores above 680 typically will get you access to best terms and rates. If your score falls below that, you will be looking at higher rates and fees, changes to down payment (or equity requirements). Beyond your score, lenders will also be looking at your history. They want to see you haven’t been late or missing any payments, had anything go to collections, or filed for consumer proposal or bankruptcy. They also want to make sure you have at least 2 credit accounts, open for 2 years or more. Having a score above 680 sometimes isn’t enough if any of these issues show up in your history.

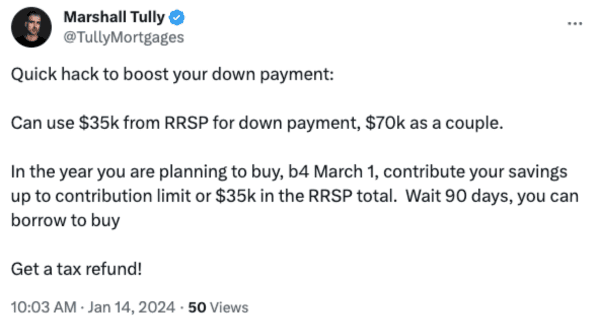

Down payment (or equity)

For home buyers, your down payment determines two things; maximum possible home price, and the type of lending you’re looking at.

For homeowners, it’s your equity that is important, and so the value of your home is going to determine the most a lender would be willing to lend against the property.

When buying a home, there are minimum requirements for down payments…

You must have 5% down for homes from $0 – $500,000.

On homes from $500k to $999k, you must have $25k (5% of $500K), plus 10% on the amount above $500k.

Example $600k house requires $35k; $25k for first $500k, plus $10k (10% of additional $100k).

Anything $1M or above, you must have 20% down.

So a purchase of $999,999 requires $75k down, and $1 more at $1M would need $200k. This can be very important.

Having less than 20% down is considered to be a ‘high risk’ mortgage in Canada, and as a result, requires the borrower to get mortgage insurance. The mortgage insurance is provided by 1 of 3 companies, all with the same or similar rules. This levels the lending playing field, as all lenders have to get you approved for insurance in the same place.

An Insurer involved means; maximum timeline for repayment of mortgage is 25 years (amortization), home value maximum of $999k, restrictions on the level of debt you can take on relative to income (more on that below), and insurance premium add to your mortgage (reduces how much is borrowed for the purchase). In other words, having less than 20% down, will negatively impact your maximum borrowing amount.

For homeowners, the value of your home will play a big role in what you can borrow. Insurance providers, as noted above, don’t cover borrowing against an existing property, that means the most you can borrow would be 80% of your current value.

As an example, if your home is worth $500k, and you owe $300k on a mortgage; you could get a new mortgage of $400k (80% of $500k), which would leave you with $100k ($400k new mortgage – $300k to pay back current mortgage).

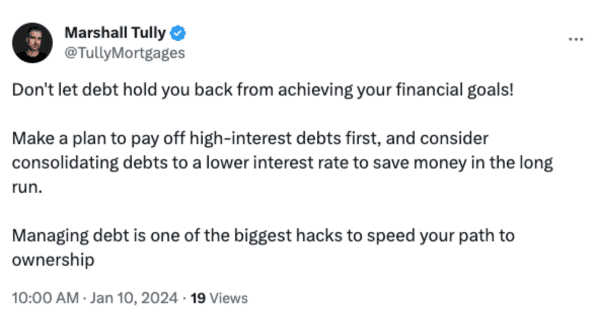

Income vs Debt

The most important piece of information in determining how much you can borrow comes down to how much you’re bringing in (income), and what you have going out (debts).

With a mortgage being a contract to repay the money over a certain period of time, what you have coming in consistently determines your ability to repay that money moving forward, hence why income is the most important factor. Here lenders will look at employment income, self-employed income, commissions, bonus, investment income, child tax benefits, child or spousal support, and more…

In addition to income, lenders are going to look at what your income can support with regards to two key areas;

- The costs of the property you are buying or refinancing

and

- The outflow of money to cover existing debt and/or other properties

When you have less than 20% down, and need insurance, they look more closely at these two numbers, and they each have a share of your income they can’t exceed. This will allow for 5% of your income to be paying existing debts, without it impacting the amount you can borrow in a mortgage. If more than 5% is going to paying current debts, this will bring down the amount of mortgage you are eligible to borrow – so you’ll want to be conscious of the debt you are carrying.

For those who have 20% down, or existing homeowners looking to borrow against there property, lenders are just concerned about the overall level of debt, so any existing debt can impact your maximum borrowing power.

The expenses that get factored in for the home, or additional properties owned, are as follows:

Mortgage Payment: The total stress-tested payment amount, payment based on 2% premium added to your rate.

Property Tax: The most recent property tax bill will confirm your annual tax amount, or will be on the listing for the property you are looking at.

Heating Cost: A monthly cost, determined based on the square-footage of the property.

Condo fees (if applicable): we include 50% of the monthly fee as an expense.

The impact, considering existing debts, are typically broken down into two categories…

Things we take actual payments for, such as: Car loans or leases, student loans, personal loans, Spousal or child support payments

Things we take 3% of outstanding balance as the monthly payment, such as: unsecured line of credit, credit cards, student line of credit

Ultimately, by eliminating, or significantly reducing your debt you are going to put yourself in the best position to qualify for a mortgage.

Be prepared, and understand what’s being looked at to ensure the best results on your next mortgage application.

Knowing what lenders are looking at, gives you control over what levers you can pull to optimize your mortgage qualification.

I hope this information can help you prepare for your next mortgage application, to best position you to achieve your goals. If you have any questions please don’t hesitate to reach out.

Overview

Subscribe to begin.

Join 7.5k+ subscribers and get tips, strategies and market updates every other Thursday morning.

")

-2")