When you tell me you want to keep the house after your separation, my first question is always the same: Have you actually run the numbers?

I’m not trying to be harsh. I’ve worked with divorcing Canadians through dozens of these buyouts over the past decade, and the reality is this: keeping your home adds a second negotiation on top of an already difficult situation.

You’re not just splitting up your life. You’re negotiating the value of your biggest asset based on appraisals, estimates, and educated guesses instead of what the market would actually pay.

That creates real risk. Someone could get a deal. Someone could get taken advantage of.

The Valuation Minefield Most People Walk Right Into

Here’s what catches people off guard: the easiest way to determine what a home is worth is to sell it on the open market. The buyer tells you exactly what it’s worth by what they’re willing to pay.

When you’re buying out your spouse, you’re relying on appraisals and broker opinions instead.

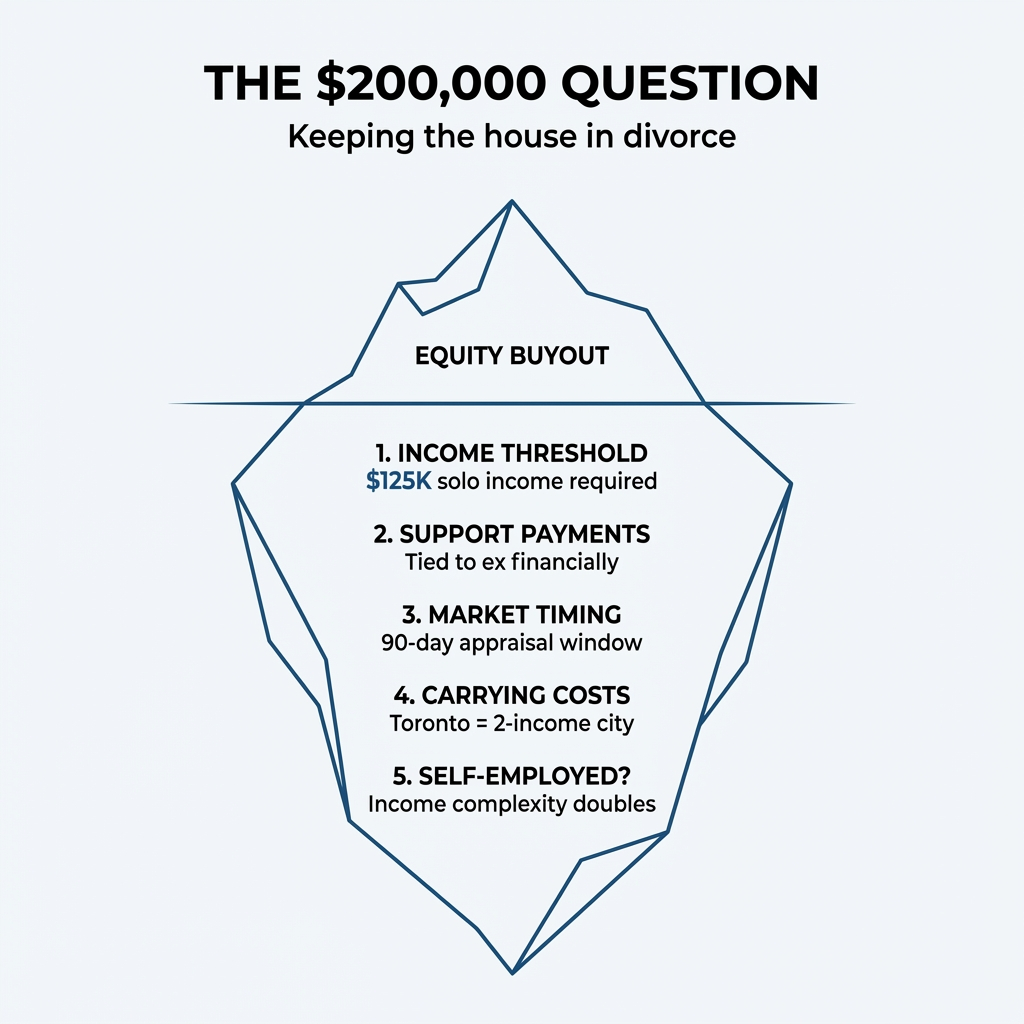

The window between valuation and closing matters more than most people realize. I’ve seen the Toronto market swing 10% or more in a matter of months, turning what seemed like a fair deal into a significant financial win or loss for one party.

The strategy that protects both parties: Get your valuation as close to the actual buyout closing date as possible. The separation process can drag on for months while you negotiate spousal support, child support, debt division, and custody arrangements. Don’t lock in a home value early in that process.

Appraisal reports are only valid for 90 days with most lenders anyway. If you ordered one early in the proceedings, you’ll need another one by closing, and if the value changed, you’re starting negotiations all over again.

My recommendation: Get multiple data points. One or two professional appraisals plus opinions from real estate agents who know your neighborhood. The more information you have, the more confident everyone can feel that you reached a fair price.

The Math That Blindsides People

Most people focus entirely on the equity payout number. That’s understandable. It’s the big, scary figure you have to come up with to buy out your spouse.

But the equity payout is just the beginning.

Let me walk you through what actually happens with a typical Toronto scenario.

You have an $800,000 home with a $400,000 mortgage. That means $400,000 in equity, split 50-50 in most cases. You owe your spouse $200,000 to buy them out.

Your new mortgage isn’t $200,000. It’s $600,000.

You need to cover the existing $400,000 mortgage plus the $200,000 buyout. To qualify for that $600,000 mortgage on your own, you need roughly $125,000 in annual income.

That’s the number that stops people cold.

In Toronto, affordability works because most households run on two incomes. When you move to a single income household, the math gets brutal fast. Add in the reality that you might be paying spousal or child support on top of that mortgage, and the required income climbs even higher.

If you’re receiving support payments, they can help you qualify, but lenders require strict documentation: a signed separation agreement outlining the amount and duration, plus 3 months of bank statements showing consistent, on-time payments.

What Happens When You Fall Short of That Income Threshold

When someone comes to me earning $90,000 or $100,000 but needs $125,000 to qualify, we don’t just give up.

As a mortgage broker, I have access to about 40 different lenders. Some traditional banks will work with extended debt-to-income ratios. Others, called B lenders, look at income and liabilities very differently than A lenders do.

How a B lender treats spousal or child support payments can reduce your debt-to-income ratio enough to make the buyout work when traditional banks say no.

But that flexibility comes with a cost.

B lenders typically charge a 2% lending fee on the total borrowing amount, plus interest rates that start about half a percentage point above A lender rates. On a $600,000 mortgage, you’re looking at $12,000 in fees upfront, plus higher monthly payments for the life of the loan.

This is where the reality check needs to happen.

The Conversation Nobody Wants to Have

A lot of people hold on to the memory of the home where they raised their kids. I understand that attachment. I’ve sat across from clients who are fighting to keep that stability, that neighborhood, that school district.

Sometimes a fresh start is what’s actually needed, both emotionally and financially.

My job is to paint as clear a picture as possible of what life will look like in your financial future. What opportunities are ahead of you. How to remove financial dependence on your ex-spouse and give yourself real freedom to reset.

Because here’s what most people don’t realize: if you’re relying on spousal or child support income to qualify for your mortgage, you’re still financially intertwined with that relationship.

Stretching yourself financially to keep the house can turn into a financial prison instead of a foundation for your next chapter.

I’ve seen it happen. Someone pushes through the buyout despite the numbers being tight. Six months later, an unexpected expense hits. A year later, they’re drowning in debt because the carrying costs were never truly sustainable on their income alone.

For many Canadians, divorce results in a 50% drop in net worth overnight. Without a solid financial plan, it can take years or even decades to recover.

That said, sometimes keeping the house makes strategic sense. Maybe you need to get your kids through their current school year before changing neighborhoods. Maybe staying close to your support network of friends matters more than the extra financial stretch. Maybe your income is about to stabilize or increase in the next year.

It’s complicated. Holding on financially to something that’s too much of a stretch will end in financial ruin and cause more stress down the road. My role is helping you assess reality and what’s actually possible.

The Self-Employed Complication

Everything gets more complicated when you’re self-employed.

A normal divorce buyout already involves negotiating equity splits, presenting clean income documentation, and managing spousal and child support calculations. When you add self-employment into the mix, you’re dealing with business equity settlements, income that doesn’t look clean on paper, potential income splitting between spouses, and tax strategies that might have changed during the separation process.

If you had spousal income splitting or joint ownership of your company, the settlement or division of the business can really impact your tax strategy. If that trickles down into reduced reported personal income, your mortgage qualification takes a hit. If it increases your income in one year, that might help with qualification, but if it’s a one-off spike, it throws off our ability to figure out if this is truly feasible for you long-term.

Separation alters your life long-term. For entrepreneurs, it can impact how you run your business, how successful that business is, and whether your income in future years makes the home affordable or unaffordable.

The Legal Requirements You Can’t Skip

Before any lender will approve a spousal buyout mortgage, you need a legally binding separation agreement. This isn’t optional.

The separation agreement outlines everything: division of the matrimonial home, child support amounts and duration, spousal support payments, debt responsibilities. Lenders rely heavily on this document to determine how much mortgage they’ll approve.

Some lenders won’t accept separation agreements drafted by mediators or templated from the internet, even if two different lawyers signed off. They require the agreement to be drafted by two separate lawyers representing each party.

The upside: having a formal separation agreement in place before buying out your spouse’s share allows you to avoid paying land transfer tax, which is a significant cost saving.

What Happens After the Buyout Closes

Most mortgage brokers treat the transaction as finished once you sign the papers and get the keys.

I don’t work that way.

I believe active debt management is the third pillar to building wealth and financial freedom, alongside earning income and investing. That’s especially true after a divorce buyout, when your financial situation is likely to keep shifting.

In the first couple years post-buyout, I’m watching for opportunities to restructure your mortgage to improve cash flow or consolidate debt. Maybe we initially went with a shorter amortization to pay down the mortgage faster, but your income stabilized lower than expected or support payments got renegotiated. We might want to extend that amortization to reduce monthly carrying costs.

Or maybe the opposite happens. Your income goes up. Support obligations end. We can speed up the amortization to pay the mortgage down quicker.

If other buyouts come up related to the separation, or unexpected expenses hit related to the kids or the ex, we might need to consolidate those debts into the mortgage to keep everything manageable.

As the dust settles post-separation, we also reassess whether the home continues to meet your needs. Sometimes what made sense emotionally in the immediate aftermath of divorce doesn’t make sense financially two years later.

The Decision Framework

Here’s what I walk every client through before they commit to a spousal buyout:

Can you actually afford it? Not just qualify for the mortgage, but truly carry the costs long-term on your solo income without relying on support payments that might change.

Have you accounted for all the costs? The equity payout, the new mortgage amount, the potential B lender fees, the ongoing maintenance and property taxes, the reality that you’ll eventually need to sell and pay real estate commissions.

Does the timeline make sense? Are you keeping the house to get through a specific period (finishing the school year, maintaining stability during a difficult transition), or are you planning to stay long-term?

What does financial freedom look like for you? Sometimes keeping the house means staying financially tied to your ex through support payments. Sometimes selling and starting fresh gives you more control and flexibility.

What are the alternatives? If traditional financing doesn’t work, are B lenders a viable option? If the numbers don’t work at all, what does selling look like?

I’ve worked with dozens of clients and families through these decisions. The ones who end up in the best financial position aren’t always the ones who kept the house. They’re the ones who made the decision based on clear-eyed assessment of the numbers and their actual long-term needs, not just the emotional pull of maintaining what was.

Divorce is already one of the hardest things you’ll go through. The last thing you need is to make it harder by turning your home into a financial burden that limits your ability to build the next chapter of your life.

If you’re facing a spousal buyout decision and want to walk through the real numbers for your specific situation, reach out. I’ll help you figure out what’s actually possible and what makes sense for your financial future.

Overview

Subscribe to begin.

Join 7.5k+ subscribers and get tips, strategies and market updates every other Thursday morning.

")

-2")